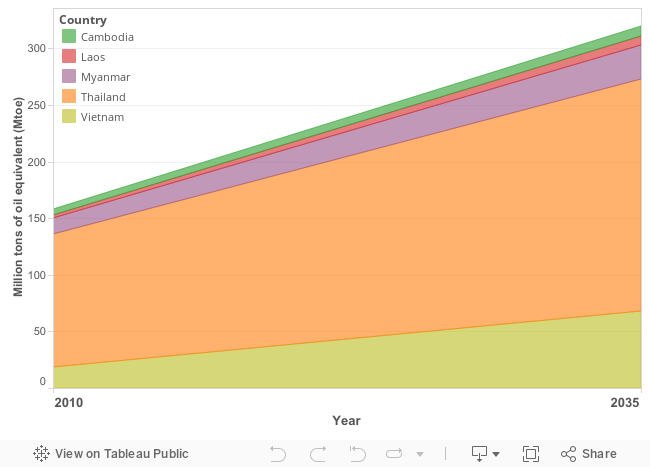

The Lower Mekong countries are hungry for energy. Between 2010 and 2035, demand is projected to double from 157.8 Mtoe (million tons of oil equivalent) to 319.6 Mtoe, concentrated heavily in Vietnam and Thailand.1 Demand will be highest for combined agriculture, commercial and residential needs, followed by industry and transport.

Projected energy demands 2010-2035

Source: Asian Development Bank, Energy Outlook for Asia and the Pacific. 2013. Created by ODI 10 June 2015. Licensed under CC BY-SA 4.0.

This increased demand has implications for energy trade and energy security within and between the Lower Mekong countries. A stable supply of clean, efficient, and cost-effective energy is therefore fundamental for sustainable economic growth and development in the region.

Energy sources

Fossil fuels (coal, oil, natural gas) remain the major energy source in the Lower Mekong countries, followed by hydropower in Cambodia, Laos and Myanmar, and biomass (firewood and charcoal) in rural areas, particularly in Cambodia. The demand for coal is projected to overtake natural gas and rise sharply to 28% of the primary energy mix by 20352. This would represent nearly one-fifth of the global growth in demand for coal. Based on current trends, the domestic demand for fossil fuels also signals increasing reliance on fuel imports. In Thailand alone, net oil and gas imports are projected to reach US$100 billion in 2035. In 2017, Thailand’s net primary energy imports were 1,430,411 barrels of oil equivalent per day.3 The country’s gas fields in the Gulf of Thailand are depleting sharply.4

Reliance on coal

A coal railway terminal in Quang Ninh, Vietnam with Qarst limestone formations in the background. Photo by garycycles8, Flickr, 12 August 2013. Licensed under CC BY 2.0.

Reliance on coal as an electricity source is increasing in the region, despite its lack of popularity elsewhere in the world. Total proven reserves of coal in the region include 3,360 million tonnes in Vietnam and 1,063 million tonnes in Thailand as at the end of 2017.5 The decline in coal prices, combined with the region’s growing demand for electricity have seen governments commit to expand coal-fired power sources, at the same time as they are committing to higher levels of renewable energy (see Energy supply below). The Vietnamese government, for example, expects coal demand to climb to 86.4 million tonnes/year by 2020 from an estimated 47.5 million tonnes in 2016.6 Thailand has plans for new coal-fired power plants in the southern provinces of Krabi (800 MW) and Thepa (2000 MW).7

Energy supply

In terms of energy supply and trade flows in the region, Laos is the largest volume exporter of electricity and the most competitively priced supplier. Thailand and Vietnam are reliant on imports from other countries, particularly from hydropower generation, to meet their rapidly growing electricity demands. Cambodia is increasing its domestic energy production but still relies on imports.8 Cambodia has the highest electricity tariffs in the region, with costs in the provinces tending to be higher than in Phnom Penh. Meanwhile, what Cambodia, Laos and Myanmar lack in domestic fossil fuel supply, they are working to make up in renewable and hydropower energy production. Laos plans to increase its share of renewables by 30% by 2025, which includes a 10% target for using biofuels in transport. Myanmar intends to increase its share of renewable power generating capacity to 18% of its energy mix by 2020.9

Access to electricity

Access to electricity varies widely, ranging from near universal access in Thailand and Vietnam at 100% and 99.2%, respectively, to 78% in Laos, 56% in Cambodia 52% in Myanmar.10 Millions of rural Cambodians depend on biomass for domestic cooking11 and automobile batteries, kerosene lamps and candles for lighting.

In the last decade, Cambodia and Laos have rolled out extensive rural electrification programs, using a combination of transmission grid extension and off-grid systems such as mini/micro hydropower, biomass gasification and solar. These have primarily followed national agendas, and contributed little to regional connectedness, leading to uneven access and distribution of energy resources and a mutual import-export dependency among the Lower Mekong countries.

Regional energy initiatives

Photovoltaic cells at Lopburi solar project, Thailand. Photo by Asian Development Bank, Flickr, 24 May 2011. Licensed under CC BY-NC-ND 2.0.

Several regional energy initiatives are aimed at addressing this issue. Of most importance is the ADB’s Greater Mekong Subregion (GMS) Energy Sub-Sector Program, which will expand national transmission grids in the GMS countries (the five Lower Mekong countries plus the Chinese provinces of Chang Du and Yunnan) to facilitate a cross-border grid network, energy market integration, and cooperation on energy security and sustainability in the region. The Lower Mekong countries are actively involved in projects associated with the GMS Energy Sub-sector Program and ASEAN’s various energy bodies under the intra-governmental ASEAN Centre for Energy (ACE).

Related to energy

References

- 1. Asian Development Bank. 2013. Energy Outlook for Asia and the Pacific. Manila, Philippines: ADB. Accessed 10 June 2015. http://adb.org/sites/default/files/pub/2013/energy-outlook.pdf.

- 2. International Energy Agency. 2013. Southeast Asia Energy Outlook. France: IEA, 37. Accessed 10 June 2015. https://www.iea.org/publications/freepublications/publication/SoutheastAsiaEnergyOutlook_WEO2013SpecialReport.pdf.

- 3. Thailand Ministry of Energy 2018. http://www.eppo.go.th/index.php/en/en-energystatistics/summary-statistic?orders[publishUp]=publishUp&issearch=1 Accessed 9 January 2018

- 4. Yuthana Praiwan 2017. “Egat plans new coal plant study”, Bangkok Post, 15 March 2017. https://www.pressreader.com/thailand/bangkok-post/20170315/281878708181054 Accessed 16 May 2017.

- 5. BP 2018. BP Statistical Review of World Energy, June 2018. https://www.bp.com/content/dam/bp/en/corporate/pdf/energy-economics/statistical-review/bp-stats-review-2018-full-report.pdf Accessed 9 January 2019.

- 6. S&P Global 2016. “Vietnam sees domestic coal demand surging nearly 80% by 2020”, Platts, 21 March 2016. https://www.platts.com/latest-news/coal/singapore/vietnam-sees-domestic-coal-demand-surging-nearly-26401582 Accessed 11 May 2017.

- 7. Yuthana Praiwan 2017. Op cit.

- 8. June, Anthony. 2013. Greater Mekong Subregion (GMS) Market Coordination. Bangkok: ADB. Paper presented at the Sustainable Energy Training, Bangkok, Thailand, 27 November. Accessed 22 July 2015. http://www.iea.org/media/training/bangkoknov13/session_9a_adb_gms_regional_market.pdf.

- 9. International Energy Agency. 2013. Southeast Asia Energy Outlook. France: IEA, 33. Accessed 10 June 2015. https://www.iea.org/publications/freepublications/publication/SoutheastAsiaEnergyOutlook_WEO2013SpecialReport.pdf.

- 10. World Bank. “Access to Electricity ( % of Population).” Accessed 11 May 2017.http://data.worldbank.org/indicator/EG.ELC.ACCS.ZS?end=2014&locations=KH-LA-MM-TH-VN&start=2000

- 11. “Cambodia Energy Situation.” Accessed 8 April 2015. https://energypedia.info/wiki/Cambodia_Energy_Situation#Energy_Situation.